Equity Matters for All Schoolchildren

School Finance Interim Charge, Testimony of IDRA – Presented by David Hinojosa, J.D., National Director of Policy before the Joint Texas House Public Education and Appropriations Committee, September 29, 2016

Thank you for allowing the Intercultural Development Research Association (IDRA) the opportunity to present written testimony of its research and analysis on school finance. Our testimony focuses on recapture, Additional State Aid for Tax Reduction (ASATR), and cost of education index (CEI).

IDRA is an independent, non-profit organization that is dedicated to assuring equal educational opportunity for every child through strong public schools that prepare all students to access and succeed in college. Since its founding in 1973, IDRA has conducted extensive research and analysis on Texas school finance, which has been used to help inform policymakers for the past five decades.

Based on its analysis described further below, and in order to achieve greater equity and efficiency in the system, IDRA recommends that the Texas Legislature consider the following:

1. Maintaining recapture but lessening its impact by:

- Enacting recapture for golden penny revenue above the Austin level and extending the number of golden pennies from six to ten pennies; also allowing local school boards to tax up to $1.10 without a tax ratification election.

- Raising the equalized wealth level for copper pennies to the same level for the basic allotment.

- Increasing the weights for bilingual (to 0.25) and compensatory education (to 0.25), which will increase the WADA and reduce the property wealth/WADA.

- Adding an inflationary rate to the basic allotment.

The State can consider paying for these measures, in part, by eliminating some of the inefficient components of its school finance system and its educational policies, including:

- Shifting revenue from the high school allotment, the available school fund and ASATR funds to increased golden pennies or copper pennies.

- Transferring available charter school funding by capping charter schools and quickly phasing out underperforming charters.

2. Avoiding measures that would increase the inequities in the system, such as increasing the number of golden pennies without recapture, eliminating the cost of education index, enacting further hold-harmless measures, and creating special provisions for a select group of districts.

3. Eliminating ASATR and the 1992-93 hold-harmless provision, or in the alternative, make it more efficient by eliminating or reducing ASATR for those districts:

- Enrolling 1600 ADA or less and generating more than $7,500/WADA; and

- Enrolling more than 1600 ADA and generating more than $7,000/WADA;

- Holding the remaining districts’ revenues per WADA constant until the school formulas make up the difference between target revenue and formula funding.

4. Enacting a statewide property tax that ensures an equitable and adequate education for all children to achieve their potential.

5. Updating the CEI to present-day values and circumstances and including educational needs-based provisions like concentration of economically disadvantaged and English learner (EL) students.

Recapture is a necessary tool for creating an efficient Texas school finance system because the state continues to rely heavily on taxes generated from grossly disparate local property values

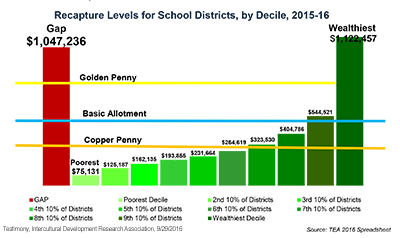

Recapture was first enacted as an essential tool for moving toward greater equity in 1993, as part of SB 7 (Cardenas, 1997). Because Texas continues to rely heavily on local property taxes and because Texas has incredibly disparate property values across the state, recapture remains an essential part of the state’s school finance system. Below is a chart showing the various recapture levels and the property values per WADA for the districts weighted by decile for the 2015-16 school year.

Key findings of IDRA’s analysis of recapture are:

- The number of districts paying recapture has risen over the last 10 years, but recapture accounts for a smaller percentage of Foundation School Program (FSP) funding over the same period. Over the last 10 years, the number of Chapter 41 districts paying recapture rose from a low of 142 in 2006 to an estimated 239 districts in 2016. However, as a percentage of the Foundation School Program (FSP), recapture has not increased over the years and remains lower than the percentage in 2006.

- Chapter 41 districts paying recapture have an estimated 12-cent tax advantage over Chapter 42 districts, even after paying recapture. A weighted analysis showed Chapter 41 districts paying recapture generating over $250/WADA more than Chapter 42 districts while paying 4¢ less in taxes. It would take property poor districts approximately an 8¢ tax hike in copper pennies to make up the difference, thus amounting to a 12¢ tax gap advantage for the wealthier districts.

- Inequities are compounded with credits for paying recapture, the unrecaptured golden pennies, and ASATR benefitting many of these same districts.

(Source: TEA Exhibit 11470, Texas Taxpayer & Student Fairness Coalition v. Morath, for 2006-2014, and TEA 2016 Spreadsheet)

As the analysis shows, recapture remains an integral part of school finance equity. Those districts subject to recapture, especially the super-wealthy districts, continue to generate significantly greater funds. Our proposals laid out above ensure greater equity in the system.

Legal Background: Recapture has been upheld three times

Several school districts attacked recapture in the courts but lost in Edgewood v. Meno (Edgewood IV). In 2005, the Supreme Court of Texas again affirmed the need for recapture stating, “Recapture helps fund the FSP and further equalizes access to revenue among districts” (Neeley v. W. Orange Cove Indep. Sch. Dist., 176 S.W.3d 746 at 759 (Tex. 2005). In response to a complaint by high-wealth school districts of the tax ratification election process and the requirement to pay recapture at the lower copper penny yield, the Supreme Court held, “Obtaining voter approval for a tax increase may pose political challenges, but we agree with the State that letting ‘local voters decide whether to raise taxes is the exact opposite of a state-imposed property tax rate’” (Texas Taxpayer & Student Fairness Coalition v. Morath at 92).

ASATR

ASATR was the latest hold-harmless measure enacted by the legislature to offset the loss in revenue for districts as a result of the phasing in of the compression of property tax rates by one-third that began in 2006-07. ASATR is set to expire following the 2016-17 school year.

IDRA analyzed the same TEA data in the spreadsheets identified in the recapture section above. Overall, we found that ASATR’s initial intent to provide a temporary stop-gap measure has been replaced by an ongoing policy that primarily benefits property-rich districts already benefitting significantly under the school finance system, regardless of educational need. These funds are not tied directly to educational need.

Key findings of IDRA’s analysis of ASATR funding:

- The number of districts receiving ASATR has fallen from a high of 1,022 in 2007 to 251 in 2016.

- Chapter 41 districts are the primary beneficiaries of ASATR, accounting for approximately 203 of the 251 ASATR districts in 2016.

- Chapter 41 districts received approximately 87 percent of total ASATR funding in 2016, compared to 27 percent in 2007.

The Texas Legislature should consider eliminating ASATR, or at the very least, reducing ASATR for those school districts that continue to receive it and already generate revenue well in excess of the statewide averages of approximately $6,500.

Available Revenue to Make System More Efficient

The Texas Legislature is concerned about how much investment is possible. Undoubtedly, closing loopholes in the franchise business tax and identifying additional funding sources for new revenues is critical. In addition, below are some areas that the state should consider:

A. Unrecaptured Revenue

Due to various provisions in the Texas Education Code, there is substantial revenue lying outside the system that is not equalized. This was estimated by TEA to be approximately $1.3 billion in 2015 (TEA Ex. 11470).

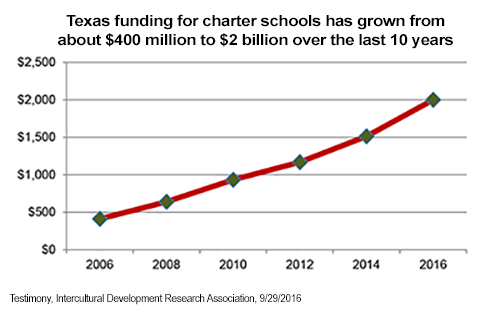

B. Charter Schools

Because charter schools do not have a local tax base from which to generate revenue, the State pays 100 percent of the Foundation School Program. And while some charter schools appear to be performing at least as good as some traditional public schools, on the whole, they are underperforming. Based on 2015 TEA reports:

- One out of every 12 charter operators (8.2 percent) failed to achieve the “met standard” or the lower “alternative standard,” compared to fewer than one out of every 25 school districts (3.8 percent).

- The true story may be even worse as 10 charters (5.1 percent) were not rated compared to only two school districts (0.2 percent)

The state’s investment in charter schools has largely not paid out, especially for many children and families hoping for better opportunities. Total FSP for charter schools has grown from approximately $400 million to $2 billion over the last 10 years, paid entirely by the State.

Placing a cap on further charter schools and closing low-performing charter schools and using those dollars to invest in traditional public schools could help free up hundreds of millions of dollars now and in the future. In addition, as more school children return to their local neighborhood schools, property values per WADA would decrease, as would recapture.

C. High School Allotment

The Texas Legislature created the High School Allotment (HSA) in 2006. Among other related purposes, the HSA was intended to prepare underachieving students for higher education and to provide opportunities for students to engage in rigorous academics. Funding amounts are based on the amount of $275 for each student in average daily attendance in grades 9 through 12. In 2016-17, the HSA is estimated to rise to $378 million (2016-17 Statewide Summary of Finances, Sep. 20, 2016). Rolling these funds into the formula system could help increase equity for all students and still allow districts to use the funds for those purposes.

D. Available School Fund (per capita distribution)

The Available School Fund (ASF) is comprised of distributions from the Permanent School Fund and motor fuels tax revenue. Funds from the ASF support the Instructional Materials Fund and a per capita distribution to school districts through the Foundation School Program. However, while ASF is rolled into formula funding for Ch. 42 districts, Ch. 41 districts receive ASF payments on top of what they generate. The ASF per capita distribution was $873 million (2015-16 Statewide Summary of Finances, Sep. 20, 2016). The Texas Legislature should explore ways to more efficiently distribute these funds in a constitutional manner.

In conclusion, as you are well aware, Texas cannot afford an excellent system for some children and a less-than-adequate system for the rest. We can and should have excellent education for all Texas school children! The future of Texas depends on it and having a fair school funding system will help deliver it.

Please know that IDRA is available to work with you and continues to be available to serve as a resource to the state legislature as you move forward at this important juncture. IDRA thanks this committee for the opportunity to testify and stands ready as a resource. If you have any questions, please contact IDRA’s National Director of Policy, David Hinojosa, at david.hinojosa@idra.org or 210-444-1710, ext. 1739.

The Intercultural Development Research Association is an independent, non-profit organization, led by María Robledo Montecel, Ph.D. Our mission is to achieve equal educational opportunity for every child through strong public schools that prepare all students to access and succeed in college. IDRA strengthens and transforms public education by providing dynamic training; useful research, evaluation, and frameworks for action; timely policy analyses; and innovative materials and programs.